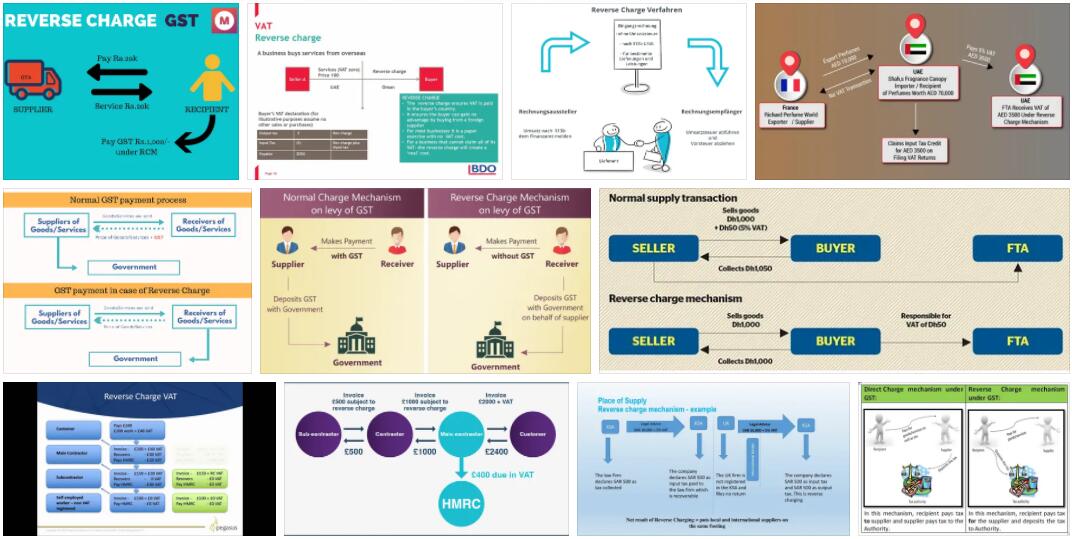

The reverse charge process is known as the reverse of the tax liability. This is a special regulation in sales tax law. It is not the entrepreneur who provides the service who pays the sales tax , but the recipient of the service must pay the sales tax. Since June 30, 2013, a corresponding invoice must be marked with the information “Tax liability of the service recipient”.

Reverse Charge Basics

Emergence

The sales tax law in Germany is based not only on national requirements, but also on the international legal provisions of the EU. These were first introduced in 1967 with the First Directive on the harmonization of the laws of the Member States on sales tax. The VAT system has thus been adapted in all Member States. The Sixth Directive has been in force since 1977. This also resulted in the reverse charge procedure, which, in accordance with Section 13 b UStG, means reversing the tax liability. That means: the recipient of the service pays the tax liability to the tax office.

Importance

According to Foodezine, sales tax law states that companies that provide the service have to pay sales tax to the tax office. The recipient of the service can deduct the sales tax as input tax if he is an entrepreneur and he has not opted for the small business regulation . The prerequisites for deducting input tax must be met.

If the sales tax liability is reversed, the recipient of the service must pay the sales tax to the tax office for certain services. In this way, the tax procedure is simplified for the tax authorities, and there is also relief for the service provider. Tax fraud in the context of sales tax is avoided with this regulation. The obligation to pay sales tax can offer advantages for the recipient of the service , because he does not have to pre-finance the sales tax that he pays to the provider of the service until it is reimbursed by the tax office.

Unfortunately, the regulation also has disadvantages, because it facilitates VAT fraud, not only in Germany, but in the entire EU. This is because the customer can offset his input tax with the tax office and is reimbursed, while the supplier does not pay his sales tax to the tax office.

Third country reverse charge

The reversal of the tax liability is not only required for EU member states, but also for some cross-border transactions in third countries. Often these are import / export deals with the United States or China.

In both cases, the sales tax between the countries concerned must be offset by the buyer and seller. When a product is sold, the invoice is issued net and the tax amount is reported to the tax authorities. The customer accepts the goods and sets off the sales tax applicable in his country on his commercial invoice.

Reverse Charge Risks

When deciding in favor of the reverse charge procedure, the provider of the service bears the risk that he will be liable for the reversal of the tax liability if the obligee does not pay the sales tax to the tax office. There is also a risk for the recipient of the service if he pays the sales tax to the service provider. In the case of reverse charge, he may not make any input tax deduction.

Use of the reverse charge procedure

Typical errors are, on the one hand, all errors that can also occur in other invoices and which make them faulty, for example if the time of performance is missing or the address details or tax number are incorrect or missing.

In addition, there are incorrect invoice corrections, i.e. cancellation invoices and newly issued invoices. The problem with all of these possible errors is that incorrect invoices are not recognized by the tax office and could ultimately lead to the loss of the input tax deduction.

It is even more common, however, that an invoice accidentally (or not at all) refers to the reverse charge procedure. If the tax liability is wrongly assigned to the recipient, but who is not taxable because there is no case of § 13 b UStG, he does not owe it. The recipient then has problems if he wants to claim input tax from this invoice at the tax office. In any case, the mistake must be resolved and corrected as quickly as possible! A reverse charge invoice template can be helpful in this case.

How reverse charge works

With the reverse charge procedure, the provider of the service may only charge his customer the net fee. To obtain the service, the customer has to pay his sales tax to the tax office. If he is entitled to deduct input tax , he can deduct the sales tax himself as input tax. There is no difference in terms of the economic burden between the reverse charge procedure and normal sales tax.

Advantages of the procedure

Reverse-Charge brings simplifications for the tax authorities and for the service provider, because the process does not have to be declared to the tax office. The reverse charge procedure is particularly useful for saving administrative work in cross-border traffic. A foreign company is saved a lot of effort with reverse charge, as it does not have to contact a German tax office. The tax authorities do not run the risk of having to enforce tax claims abroad.